Retirement Spending Smile”: What Aging Adults Need to Know

With a new year, we often think about resolutions and making new plans. If your preference is to age independently in the place you call home, then planning for financial security is critically important.

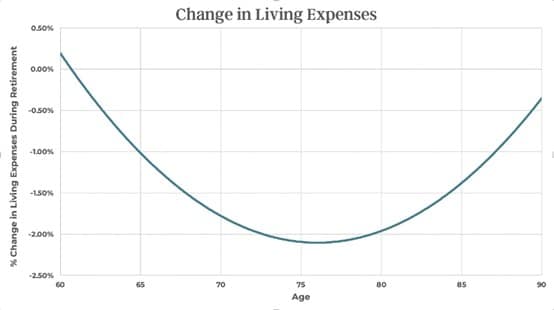

Planning for retirement isn’t just about saving enough. It’s also about understanding how your spending will change over time. Research shows that retirees don’t spend in a straight line. Instead, spending tends to start high, dip in the middle years, and rise again later in life. This pattern forms what experts call the “retirement spending smile.”

For Baby Boomers and Gen Xers who are not yet Friends Life Care members, this insight is important to consider. Friends Life Care’s Continuing Care at Home program can help members be better prepared with a plan in place for the future. This is a good step towards having the retirement lifestyle you want, while ensuring you have resources that can pay for care and support as you age at home.

What is the “Spending Smile”

If you’ve ever tried to build a retirement budget, you may have been told to plan on spending the same amount every year—just adjust for inflation. Reality likely looks different. A growing body of research shows that retiree spending tends to start high, dip in the middle retirement years, and rise again later in life, particularly due to health care.

Health care spending rises significantly after age 80. J.P. Morgan estimates monthly health care costs can triple between age 65 and 95. For those aging in place, this often means more home health services, adaptive equipment, and medication management.

This forms a curve that looks like a smile.

What the Experts Are Saying

“Retiree expenditures do not, on average, increase each year by inflation… the actual ‘spending curve’ of a retiree household varies by total consumption and funding level.” — David Blanchett, Head of Retirement Research (Morningstar)

The Head of Planning Strategy at Focus Partners Wealth, Michael Kitces talks about three different phases of retirement and aging: the go-go years, the slow-go years, and the no-go years. He further explains “Real retiree spending decreases slowly in the early years, more rapidly in the middle years, and then less slowly in the final years… a path that looks less like a slow and steady decline and more like a ‘retirement spending smile.’” — Michael Kitces

Three Phases of Aging

The smile chart and different phases of aging directly affect Baby Boomers and Gen Xers through the retirement years. This section will dig deeper into how it shows up in real life and things you can do to put a plan in place that fits your lifestyle.

As mentioned, the smile chart reflects three broad phases:

- Early retirement (the “go‑go” years): Spending often climbs as new retirees travel, dine out, update homes, and invest in hobbies.

- Mid‑retirement (the “slow‑go” years): Activity and discretionary spending tend to taper; inflation‑adjusted total spending declines.

- Late retirement (the “no‑go” years): Health‑related costs rise and may push spending up again—creating the right side of the smile.

Why the Smile Matters (and Why It’s Good News)

The traditional assumption — that retirees must inflate spending each and every year through all of retirement — can overestimate what you need to retire.

For Boomers already retired or near retirement, and Gen Xers building toward it, this can be empowering: with the  right plan, you may be able to enjoy more in the early years without jeopardizing long‑term sustainability.

right plan, you may be able to enjoy more in the early years without jeopardizing long‑term sustainability.

Vanguard, for example, encourages dynamic spending—flexing withdrawals with markets and life phase—to help retirees “spend more” sustainably than outdated and rigid rules had allowed.

You’ve worked hard to build your nest egg. The smile chart and the experts that did the research to create it are not telling anyone to spend recklessly.

Rather, they are explaining that retirees can spend more intentionally when they understand the phases of aging. With this, you can decide to front‑load joy when you’re most able to enjoy it “go-go” years. Then you may anticipate a natural dip “slow-go” years. And ultimately, it is important to be well prepared for health care later “no-go” years.

How to Plan for the Smile and Stay at Home

- Create a Phase-Based Budget: Plan for early lifestyle spending, mid-life stability, and late-life care.

- Consider Continuing Care at Home: Programs like Friends Life Care provide a safety net to help pay for care and support without moving to a facility.

- Build Flexibility: Dynamic spending strategies let you enjoy early retirement while protecting long-term security.

- Prepare for Health Care: Medicare alone won’t cover everything. Friends Life Care fills the gaps with wellness and care coordination and financial protection.

More About Continuing Care at Home Plans

And membership in a continuing care at home plan can be a useful part of the mix. Why? Because you have access to a bundle of services that are important ingredients to aging in place: wellness and care coordination, recommendations for home accessibility and safety, concierge services for home and life, financial security, and more. These services and supports are with you through all the phases of aging.

Ready to Learn More?

If you’re a Senior, Baby Boomer or Gen Xer who is already retired, semi-retired or planning for retirement, now is the time to explore Friends Life Care’s program. It’s the smart way to secure your future, protect your independence, and make the most of every phase of retirement.

Contact Friends Life Care today to schedule a consultation and discover how you can age in place with confidence.

Leave a Comment